Construction doesn’t stall because everyone agreed. It stalls because someone didn’t perform. That is the simple reason performance bonds exist. They give owners a practical remedy when a contractor fails to complete the work as promised. If you build, finance, or manage projects, understanding how performance bonds intersect with subcontractor bonds and flow-down clauses is not optional. It is core risk management.

A working definition that matters on site

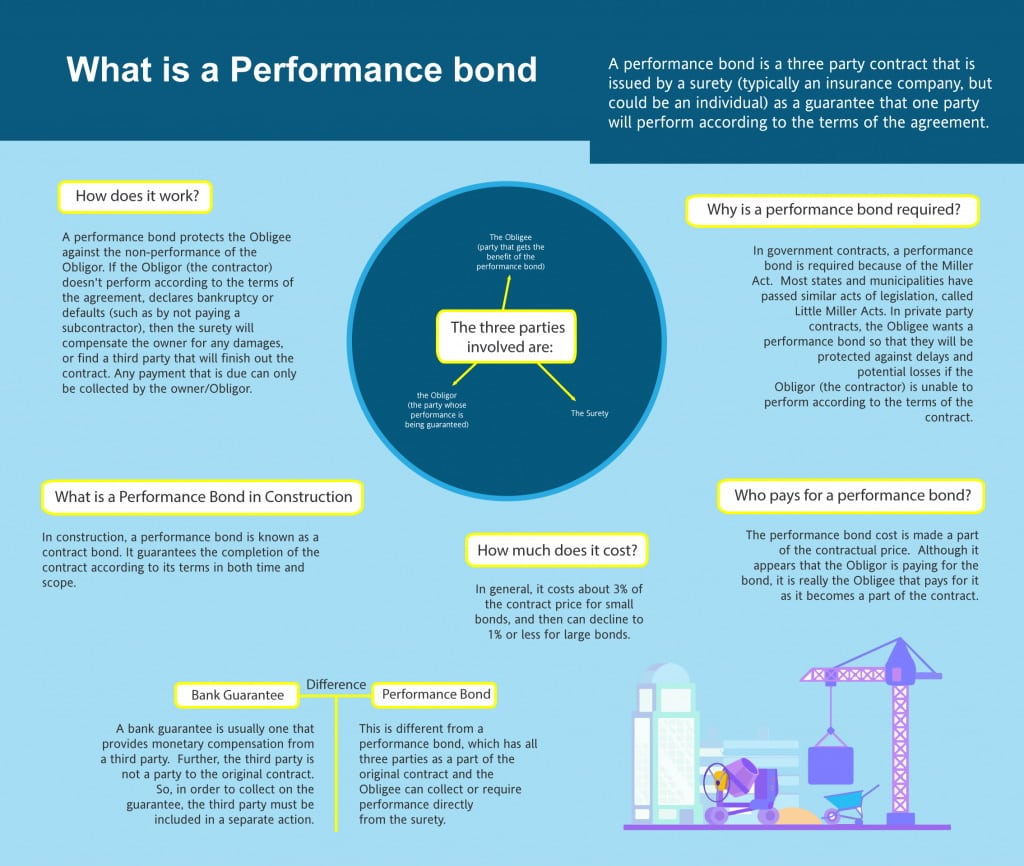

A performance bond is a three-party agreement where a surety guarantees that a bonded contractor will finish the project according to the contract. If the contractor defaults, the surety steps in to remedy the default up to the penal sum of the bond, typically 100 percent of the contract price. For public work in the United States, performance bonds are often mandated by the Miller Act at the federal level and by “Little Miller” acts in most states. On private work, they are negotiated based on the owner’s risk appetite, lender requirements, and contractor qualifications.

It helps to visualize the roles. The owner is the obligee who benefits from the bond. The contractor is the principal who must perform the underlying contract. The surety is a regulated financial company that underwrites the principal’s capacity and stands behind it. The surety is not an insurer in the ordinary sense. It expects the contractor to reimburse any loss and it typically requires personal and corporate indemnity. That subtle shift in incentives matters. Insurers price for expected losses, while sureties underwrite to avoid them.

Contractors often ask what is a performance bond really protecting. It protects the owner’s interest in getting the job completed per the contract, not the contractor’s margin. It is not a warranty bond, though completion may include correcting defective work. It does not guarantee that the contractor will never default. It provides a defined path to finish the project if default occurs.

Common triggers and the surety’s options

Default is a contract-defined event. Typical triggers include abandonment of the work, chronic failure to meet schedules, refusal to correct defective work, insolvency, or a material breach such as nonpayment to subs that disrupts progress. Owners must tread carefully here. Calling a default prematurely, or failing to follow notice and cure procedures, can discharge the surety’s obligations. I once watched a municipal owner issue a termination for convenience letter out of frustration, then try to demand performance under the bond. The surety treated the convenience termination as the owner’s election, not a contractor default, and the claim went nowhere. Procedure matters.

If a valid default occurs and the owner declares the contractor in default and formally tenders the project to the surety, the surety has several avenues:

- Finance the existing contractor to complete the work under enhanced oversight. Tender a replacement contractor acceptable to the owner and fund the shortfall. Enter into a takeover agreement and manage completion itself through a completion contractor. Pay the obligee up to the penal sum and walk away, leaving the owner to self-manage completion.

The path chosen depends on the facts on the ground: percent complete, cost to complete, quality of the records, and whether critical subs are still available. If the project is 85 percent complete with clean documentation and cooperative subs, financing the original contractor can be fastest. If the contractor is insolvent and the relationships are poisoned, a tendered or takeover completion may be wiser.

What owners expect versus what bonds actually deliver

Owners tend to imagine bonds as a turnkey rescue. In practice, a bond is a structured safety net with friction. The surety must investigate, verify default, and quantify the remaining cost to complete. That investigation is not a stall tactic, it is a legal obligation. On complex commercial or heavy civil work, the investigation phase can run several weeks. Time is money, so the owner’s goal should be to make the investigation efficient: clean schedules of values, updated CPM schedules, substantiated change orders, current lien waivers, and a clear record of notices.

There are also coverage boundaries. The penal sum caps the surety’s liability. If the owner has approved significant scope changes without corresponding bond increases, the surety can argue for a proportional cap or even discharge. Liquidated damages may be covered up to the penal sum, but acceleration costs beyond reasonable mitigation may not be, especially where the owner contributed to delays. The bond is not a blank check to solve every project woe.

The cost of a performance bond and what drives it

Bond premium usually lands between 0.5 and 3 percent of the contract price, tiered by size and risk. Large, straightforward projects performed by a well-capitalized contractor with a clean record may price at the low end. Heavier risk profiles push the rate higher. Underwriters examine working capital, backlog, project type, and management depth. Specialty work with narrow vendor pools or volatile materials can push rates and capacity constraints. I have seen a $50 million process facility with a welded stainless scope get priced above 2 percent because the completion risk for that specialty labor could not be easily transferred.

One mistake owners make is treating the bond premium as wasted overhead. It is more accurate to see it as part of the project’s risk pricing. A bonded low bid can be lower on paper while still offering stronger completion security than an unbonded slightly higher bid. Conversely, there are projects where the owner knows the contractor intimately, has step-in rights through funding agreements, and maintains a controlled payment process. On those jobs, a full performance bond may be overkill compared to a parent guarantee or a letter of credit. The right instrument fits the commercial relationship and the path to completion if something goes wrong.

Payment bonds ride alongside

On most public and many private projects, performance bonds travel with payment bonds. The payment bond protects subcontractors and suppliers who furnish labor and materials but cannot file mechanics liens on public property. Even where liens are available on private work, lenders often insist on payment bonds to prevent lien filings that can cripple financing. For field-level operations, the payment bond smooths procurement and keeps critical vendors engaged when the prime contractor is wobbling. If you are an owner, requiring both bonds keeps the pipeline of materials and the goodwill of subs intact during turbulence.

Where subcontractor bonds fit

Subcontractor default is the most common operational failure on complex builds. Mechanical, electrical, and structural steel subs carry disproportionate critical path risk. A prime can meet every deadline on paper and still miss the project if a key sub cannot staff or finance its phase. Subcontractor performance bonds, also called “sub-bonds,” are one way primes manage that exposure.

A sub-bond mirrors the structure of the prime bond. The obligee is the general contractor, the principal is the subcontractor, and the surety guarantees the sub’s performance up to the penal sum, often 100 percent of the subcontract value. On a hospital project I worked, the electrician bonded its $18 million subcontract. When copper prices spiked and retained cash tightened, the sub fell behind. The surety financed payroll during a planned re-sequencing and kept the same crews in place. The project dodged a six-month delay that a replacement would have caused.

Sub-bonds come with trade-offs. They increase the subcontractor’s cost and tie up surety capacity. For midsize subs, bonding too much backlog can choke future opportunities. They also can give primes a false sense of security if the sub-bond penal sum is inadequate or if the default provisions in the subcontract do not align with the bond’s requirements for notice and opportunity to cure. The best practice is to target bonding to trades with high completion risk and to ensure the subcontract and the bond speak the same language about defaults, schedules, and change orders.

Flow-down clauses set the rules of the road

Flow-down clauses push prime contract obligations downstream into subcontracts. They can be broad, making the entire prime contract applicable to the sub as if the sub had signed it, or they can be selective, incorporating only specific provisions such as schedule, quality standards, insurance, safety, dispute resolution, or liquidated damages. Flow-downs exist because the owner’s expectations do not evaporate at the prime’s ledger. If the prime must meet a Guaranteed Maximum Price with defined alternates, the subs providing those alternates must live within the same guardrails.

From a bonding standpoint, flow-downs are not law-school trivia. Sureties care about the contract terms they are backing. If a prime bond requires strict notice windows for claims and changes, and the sub’s bond does not mirror those windows, you create timing mismatches that are hard to navigate during a default. A disciplined subcontract aligns with the prime on key mechanics: documentation standards, schedule integration, change management, termination and default procedures, and dispute resolution forum and timing. When the documents mesh, the surety’s path to cure is clearer and faster.

The interplay: prime bond, sub-bond, and flow-down

Consider a mid-rise residential build. The prime contract requires a performance and payment bond from the general contractor, includes a 15 swiftbonds percent retainage cap, sets liquidated damages at $5,000 per day, and mandates arbitration in a defined city. The general contractor subcontracts concrete, framing, and MEP. It requires performance bonds from the concrete and MEP subs, declines to bond framing given the contractor’s long relationship with that shop, and uses a subcontract that flows down schedule, LD exposure, and dispute resolution.

At month nine, the concrete sub’s formwork vendor files for bankruptcy, the crew misses several placements, and slab pours slip. The general issues a cure notice under the subcontract, gives seven days to propose a recovery plan, and copies the surety. The recovery plan is thin and cash flow problems surface. The general declares a default and tenders the subcontract to the surety. Because the subcontract mirrors the prime’s notice and default terms, the surety steps into a familiar framework, finances a replacement formwork vendor, and accelerates weekend pours. The project still eats four weeks of schedule float, but LD exposure is contained and the prime’s bond is never called. The alignment of documents saved months of wrangling.

Flip the facts. Suppose the subcontract lacked a clear flow-down of LDs and schedule obligations, and the sub-bond referenced a different default and cure period from the prime. Now the general faces LDs under the prime while arguing with the sub’s surety about whether default was properly triggered. Meanwhile, the critical path continues to bleed. Misalignment costs time first, then money.

Default mechanics and the importance of precision

Default under a performance bond is a legal conclusion built from contract facts. It unfolds step by step: notice of defect or delay, an opportunity to cure, documentation that the cure failed, a formal declaration of default, and a tender to the surety. Each step has timing and content requirements. Skipping a step or combining two steps into a frustrated letter can invite a denial. I have reviewed claim files where the owner attached a dozen emails complaining about progress, but never sent a contract-defined notice to cure. The surety used that gap to slow-walk the investigation, and the project lost a month before a proper notice went out.

It helps to assign a claim file owner on day one, long before any trouble starts. That person tracks notices, maintains a running index of schedule updates, logs RFI and change order status, and keeps payment and lien waiver records clean. When a default looms, the claim file owner’s work trims weeks from the surety’s diligence and deconflicts arguments about responsibility and quantum.

How lenders view bonds, subs, and flow-downs

Construction lenders live on predictability. They want an executable path to completion even if the borrower and the contractor struggle. Performance and payment bonds provide an off-ramp from chaos. Lenders often require evidence that major subs are prequalified, that the prime will bond its contract, and that subcontracts are drafted with enforceable flow-down provisions. Some lenders go further and require step-in rights or collateral assignments of subcontracts so they can direct the prime or the surety to proceed.

From a borrowing perspective, satisfying lender requirements early improves draw processing. Banks and funds will hold back on disbursements if Find out more they sniff document mismatch. Clear flow-downs, bonded high-risk subs, and a realistic schedule narrative can shave weeks off closing and keep cash flowing during construction.

Practicalities from the field

Several nuts-and-bolts practices make the difference between a smooth surety engagement and a standoff:

- Keep the schedule credible. A living CPM schedule, updated with actuals and logic checks, beats a glossy baseline. Sureties and completion contractors rely on it to forecast cost to complete and to plan recovery. Align change management. A flood of verbal directives without documented change orders is poison during a claim. If the field needs to move, issue a written directive and reserve pricing, then true-up quickly. Monitor subcontractor health. Quarterly reviews of manpower plans, look-ahead schedules, and aging reports catch trouble early. Most sub-bond defaults start as cash flow stress that shows up in pay-app slippage and vendor calls. Manage retainage intelligently. Retainage is leverage. Release too early and you reduce your remedies. Hold beyond contract terms and you risk a breach that clouds default rights. Keep communication formal when needed. Friendly emails are fine, but when risk rises, switch to contract notices with the right recipients and timing. Do not bury a notice inside a meeting recap.

When a bond may not be the right tool

Performance bonds are powerful, but not universal. On very small projects, the administrative load and premium can exceed the benefit, especially if the owner has a direct relationship with a small contractor whose entire crew is local and known. On highly specialized EPC projects where design risk, process guarantees, and long-lead equipment dominate, owners sometimes prefer letters of credit, parent guarantees from investment-grade sponsors, or escrowed reserves tied to performance milestones. Those instruments can be faster to draw and can avoid disputes about default triggers, but they require careful drafting to avoid unintended exposures.

There are also hybrid approaches. An owner might require a performance bond for the base building but use equipment supplier guarantees and liquidated damages for the process package. Or a general contractor might decline sub-bonds on low-risk trades and instead invest in a subcontractor default insurance policy that spreads risk across the portfolio while maintaining some flexibility on individual jobs. These are judgment calls, and they pay off when based on an honest assessment of failure modes, not habit.

Drafting details that prevent grief

Trouble often hides in the short clauses, not the big ones. A few drafting details make or break enforceability:

- Tie the penal sum to the evolving contract value. If you expect significant change orders, require bond increases proportional to approved changes, with a clear trigger and timing. Harmonize dispute provisions. If the prime contract requires arbitration in a specific venue, say so in the subcontract and the sub-bond. Mixed forums waste time. Define default with examples and references. Incorporate schedule lag thresholds, quality metrics, and specific documentation failures as defaults to reduce gray zones. Specify the cure period clearly and keep it reasonable. Seven to fourteen days is common for non-life-safety issues, with immediate cure allowed for safety violations. Confirm indemnity and collateral rights with the contractor’s surety. If the contractor’s surety requires consent for assignment of subcontracts in a takeover, say so upfront so no one is surprised at the worst moment.

A note on claims timing and mitigation

Owners sometimes assume calling the bond will move faster than working with the existing contractor. That is not always true. If the contractor is stumbling but cooperative, and the surety is willing to finance completion, a structured workout can outrun a replacement. The surety prefers this route because it controls costs and leverages existing knowledge on site. The owner benefits from speed. The trade-off is accepting the contractor that failed under enhanced supervision. When the failure is rooted in poor management rather than a one-time shock, a takeover with a new completion contractor may yield a cleaner finish even if it takes longer to mobilize.

Mitigation is an owner’s duty regardless of the path chosen. If winter weather is coming and temporary heat will avoid freeze damage, buy it and document it. Reasonable mitigation expenses are commonly recoverable within the bond’s penal sum. Unreasonable acceleration or speculative backcharges are not.

How to talk about bonds with your team and counterparties

Bonds sit at the junction of legal, financial, and operational disciplines. The teams that handle them well demystify the subject and keep the paperwork clean. Make sure project executives, project managers, and contract administrators share a glossary. Do not assume the field understands what a cure notice means or why an RFI log can play into a bond claim. Train a few people to build a claim file while everyone else builds the job. When subs push back on sub-bonds or flow-downs, explain the why and offer alternatives: smaller penal sums for lower-risk scopes, bonding only long-lead or business-critical phases, or offering early retainage release in exchange for a bond on later phases.

The simplest way to take the tension out of bond conversations is to tie them to outcomes: the owner wants certainty of completion, the general wants to avoid a catastrophic default, and the subs want predictable pay and a fair process. Properly structured bonds and coherent flow-downs give all three more predictability.

Answering the core question plainly

If someone corners you on site and asks what is a performance bond, tell them it is a guarantee from a third party that the contractor will finish the job as promised, and if the contractor does not, the third party will pay to finish up to the bond amount. Add that it is not magic. It works best when the contract documents are aligned, the notices are clean, and the subcontractors are either bonded or carefully managed with flow-down terms that match the prime contract.

Final thoughts from lived experience

Projects run on trust until they run on documents. Performance bonds, subcontractor bonds, and flow-down clauses are the documents that carry a project when trust wobbles. They are not there to replace good management, only to backstop it. The best outcomes I have seen shared the same pattern: selective use of sub-bonds on trades that can sink the schedule, meticulous alignment between prime and subcontracts, early and formal notice when performance falters, and a candid working relationship with the surety that starts before trouble hits. When the day comes that you need the bond, you will be glad you invested in that groundwork.